No Man is an Island: The Impact of Neighborhood Disadvantage on Mortality

Abstract

:1. Introduction

2. Materials and Methods

2.1. Data

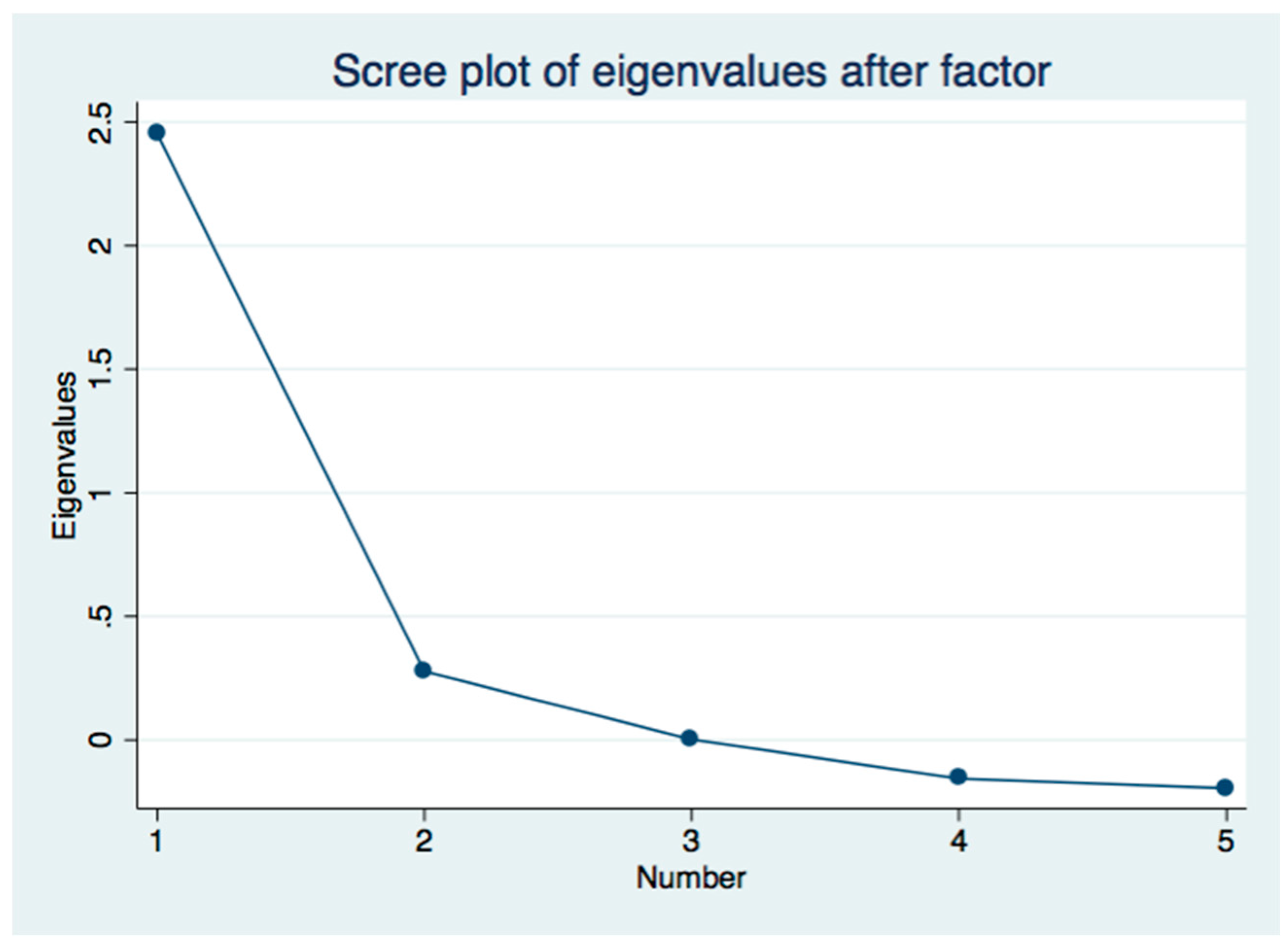

2.2. Measuring Neighborhood Disadvantage

2.3. Statistical Analysis

3. Results

3.1. Description of the Sample

3.2. Association of Neighborhood Disadvantage and Other Variables

4. Discussion

5. Conclusions

Author Contributions

Funding

Acknowledgments

Conflicts of Interest

References

- Graham, G.O.; Strowski, M.; Sabina, A. Defeating the ZIP Code Health Paradigm: Data, Technology, and Collaboration are Key. Health Affairs Blog. 6 August 2015. Available online: https://www.healthaffairs.org/do/10.1377/hblog20150806.049730/full/ (accessed on 7 February 2019). [CrossRef]

- Roux, A.V.; Merkin, S.S.; Arnett, D.; Chambless, L.; Massing, M.; Nieto, F.J.; Sorlie, P.; Szklo, M.; Tyroler, H.A.; Watson, R.L. Neighborhood of residence and incidence of coronary heart disease. N. Engl. J. Med. 2001, 345, 99–106. [Google Scholar] [CrossRef] [PubMed]

- Diez-Roux, A.V. Residential environments and cardiovascular risk. J. Urban Health. 2003, 80, 569–589. [Google Scholar] [CrossRef] [Green Version]

- Chang, V.W. Racial residential segregation and weight status among US adults. Soc. Sci. Med. 2006, 63, 1289–1303. [Google Scholar] [CrossRef]

- Kershaw, K.N.; Osypuk, T.L.; Do, D.P.; De Chavez, P.J.; Diez-Roux, A.V. Neighborhood-level racial/ethnic residential segregation and incident cardiovascular disease: The multi-ethnic study of atherosclerosis. Circulation 2015, 131, 141–148. [Google Scholar] [CrossRef]

- Murray, C.J.; Kulkarni, S.C.; Michaud, C.; Tomijima, N.; Bulzacchelli, M.T.; Iandiorio, T.J.; Ezzati, M. Eight Americas: Investigating mortality disparities across race, counties, and race-counties in the United States. PLoS Med. 2006, 3, e545. [Google Scholar]

- Chetty, R.; Stepner, M.; Abraham, S.; Lin, S.; Scuderi, B.; Turner, N.; Cutler, D. The association between income and life expectancy in the United States, 2001–2014. JAMA 2016, 315, 1750–1766. [Google Scholar] [CrossRef]

- Baltimore City Health Department. Life Expectancy at Birth, in Years, by Community Statistical Area. 2013. Available online: http://health.baltimorecity.gov/sites/default/files/Life-expectancy-2013.pdf (accessed on 6 February 2019).

- Diez-Roux, A.V.; Mair, C. Neighborhoods and health. Ann. N. Y. Acad. Sci. 2010, 1186, 125–145. [Google Scholar] [CrossRef] [PubMed] [Green Version]

- Peng, R.D.; Bell, M.L.; Geyh, A.S.; McDermott, A.; Zeger, S.L.; Samet, J.M. Emergency admissions for cardiovascular and respiratory diseases and the chemical composition of fine particle air pollution. Environ. Health Perspect. 2009, 117, 957–963. [Google Scholar] [CrossRef] [PubMed]

- Chan, K.S.; Roberts, E.; McCleary, R.; Buttorff, C.; Gaskin, D.J. Community characteristics and mortality: The relative strength of association of different community characteristics. Am. J. Public Health. 2014, 104, 1751–1758. [Google Scholar] [CrossRef] [PubMed]

- Cohen, D.A.; Mason, K.; Bedimo, A.; Scribner, R.; Basolo, V.; Farley, T.A. Neighborhood physical conditions and health. Am. J. Public Health 2003, 93, 467–471. [Google Scholar] [CrossRef] [PubMed]

- Harrison, R.A.; Gemmell, I.; Heller, R.F. The population effect of crime and neighbourhood on physical activity: An analysis of 15,461 adults. J. Epidemiol. Community Health. 2007, 61, 34–39. [Google Scholar] [CrossRef]

- Billimek, J.; Sorkin, D.H. Self-reported neighborhood safety and non-adherence to treatment regimens among patients with type 2 diabetes. J. Gen. Intern. Med. 2012, 27, 292–296. [Google Scholar] [CrossRef]

- Estabrooks, P.A.; Lee, R.E.; Gyurcsik, N.C. Resources for physical activity participation: Does availability and accessibility differ by neighborhood socioeconomic status? Ann. Behav. Med. 2003, 25, 100–104. [Google Scholar] [CrossRef]

- Ludwig, J.; Sanbonmatsu, L.; Gennetian, L.; Adam, E.; Duncan, G.J.; Katz, L.F.; Kessler, R.C.; Kling, J.R.; Lindau, S.T.; Whitaker, R.C.; et al. Neighborhoods, obesity, and diabetes--a randomized social experiment. N. Engl. J. Med. 2011, 365, 1509–1519. [Google Scholar] [CrossRef]

- Ludwig, J.; Duncan, G.J.; Gennetian, L.A. Neighborhood effects on the long-term well-being of low-income adults. Science. 2012, 337, 1505–1510. [Google Scholar] [CrossRef]

- Chetty, R.; Hendren, N.; Katz, L.F. The effects of exposure to better neighborhoods on children: New evidence from the Moving to Opportunity experiment. Am. Econ. Rev. 2016, 106, 855–902. [Google Scholar] [CrossRef]

- Chetty, R.; Hendren, N. The impacts of neighborhoods on intergenerational mobility I: Childhood exposure effects. Q. J. Econ. 2018, 133, 1107–1162. [Google Scholar] [CrossRef]

- Chetty, R.; Hendren, N. The impacts of neighborhoods on intergenerational mobility II: County-level estimates. Q. J. Econ. 2018, 133, 1163–1228. [Google Scholar] [CrossRef]

- Harris, T.F.; Yelowitz, A. Racial Disparities in Life Insurance Coverage. 28 April 2015. Available online: http://ssrn.com/abstract=2600328 (accessed on 8 April 2019).[Green Version]

- Jenkinson, C. Comparison of UK and US methods for weighting and scoring the SF-36 summary measures. J. Public Health Med. 1999, 21, 372–376. [Google Scholar] [CrossRef] [Green Version]

- Barber, S.; Hickson, D.A.; Wang, X.; Sims, M.; Nelson, C.; Diez-Roux, A.V. Neighborhood disadvantage, poor social conditions, and cardiovascular disease incidence among African American adults in the Jackson Heart Study. Am. J. Public Health 2016, 106, 2219–2226. [Google Scholar] [CrossRef]

- Singh, G.K. Area deprivation and widening inequalities in US mortality, 1969–1998. Am. J. Public Health 2003, 93, 1137–1143. [Google Scholar] [CrossRef]

- Kind, A.J.; Jencks, S.; Brock, J.; Yu, M.; Bartels, C.; Ehlenbach, W.; Smith, M. Neighborhood socioeconomic disadvantage and 30-day rehospitalization: A retrospective cohort study. Ann. Intern. Med. 2014, 161, 765–774. [Google Scholar] [CrossRef]

- Schafer, J.L. Multiple imputation: A primer. Stat. Methods Med. Res. 1999, 8, 3–15. [Google Scholar] [CrossRef]

- White, I.R.; Royston, P. Imputing missing covariate values for the Cox model. Stat. Med. 2009, 28, 1982–1998. [Google Scholar] [CrossRef] [Green Version]

- Szreter, S.; Woolcock, M. Health by association? social capital, social theory, and the political economy of public health. Int. J. Epidemiol. 2004, 33, 650–667. [Google Scholar] [CrossRef]

- Isaacs, S.L.; Schroeder, S.A. Class—The ignored determinant of the nation’s health. N. Engl. J. Med. 2004, 351, 1137–1142. [Google Scholar] [CrossRef]

- Shmueli, H.; Rogowski, O.; Toker, S.; Melamed, S.; Leshem-Rubinow, E.; Ben-Assa, E.; Shapira, I.; Berliner, S.; Steinvil, A. Effect of socioeconomic status on cardio-respiratory fitness: Data from a health screening program. J. Cardiovasc. Med. (Hagerstown) 2014, 15, 435–440. [Google Scholar] [CrossRef]

- Pollack, C.E.; Lynch, J. Health status of people undergoing foreclosure in the Philadelphia region. Am. J. Public Health. 2009, 99, 1833–1839. [Google Scholar] [CrossRef]

- Samet, J.M.; Dominici, F.; Curriero, F.C.; Coursac, I.; Zeger, S.L. Fine particular air pollution and mortality in 20 U.S. cities, 1987–1994. N. Engl. J. Med. 2000, 343, 1742–1749. [Google Scholar] [CrossRef]

- Puett, R.C.; Hart, J.E.; Yanosky, J.D.; Paciorek, C.; Schwartz, J.; Suh, H.; Speizer, F.E.; Laden, F. Chronic fine and coarse particulate exposure, mortality, and coronary heart disease in the Nurses’ Health Study. Environ. Health Perspect. 2009, 117, 1697–1701. [Google Scholar] [CrossRef]

- Eftim, S.E.; Samet, J.M.; Janes, H.; McDermott, A.; Dominici, F. Fine particulate matter and mortality: A comparison of the six cities and American Cancer Society cohorts with a Medicare cohort. Epidemiology 2008, 19, 209–216. [Google Scholar] [CrossRef]

- Pope, C.A., 3rd; Burnett, R.T.; Thun, M.J.; Calle, E.E.; Krewski, D.; Ito, K.; Thurston, G.D. Lung cancer, cardiopulmonary mortality, and long-term exposure to fine particulate air pollution. JAMA 2002, 287, 1132–1141. [Google Scholar] [CrossRef]

- Pope, C.A., 3rd; Burnett, R.T.; Thurston, G.D.; Thun, M.J.; Calle, E.E.; Krewski, D.; Godleski, J.J. Cardiovascular mortality and long-term exposure to particulate air pollution: Epidemiological evidence of general pathophysiological pathways of disease. Circulation 2004, 109, 71–77. [Google Scholar] [CrossRef]

- O’Neill, M.S.; Veves, A.; Sarnat, J.A.; Zanobetti, A.; Gold, D.R.; Economides, P.A.; Horton, E.S.; Schwartz, J. Air pollution and inflammation in type 2 diabetes: A mechanism for susceptibility. Occup. Environ. Med. 2007, 64, 373–379. [Google Scholar] [CrossRef]

- Environmental Protection Agency. The National Ambient Air Quality Standards for Particle Pollution, Revised Air Quality Standards for Particle Pollution and Updates to the Air Quality Index (AQI). 2012. Available online: http://www.epa.gov/airquality/particlepollution/2012/decfsstandards.pdf (accessed on 26 March 2015).

{kind=link}

| Individual Level Measures | Percent | Cumulative Percent |

|---|---|---|

| Income < 28,000 | 14.20 | 14.20 |

| $28,000 to 40,000 | 12.74 | 26.94 |

| $40,000 to 54,000 | 18.16 | 45.10 |

| $54,000 to 75,000 | 17.15 | 62.26 |

| $75,000 to 120,000 | 18.98 | 81.24 |

| Greater than 120,000 | 18.76 | 100.00 |

| Occupational Status | ||

| Manager | 15.75 | 15.75 |

| Financial | 4.19 | 19.94 |

| Science | 3.64 | 23.58 |

| Law/Social | 2.59 | 26.17 |

| Education | 4.57 | 30.74 |

| Protective Services | 1.24 | 31.98 |

| Health | 5.77 | 37.75 |

| Entertainment | 1.10 | 38.84 |

| Sales | 5.85 | 44.69 |

| Labor | 9.94 | 54.64 |

| Service | 4.10 | 58.74 |

| Not working | 1.24 | 59.98 |

| Other | 40.02 | 100.00 |

| Individual Characteristics | Mean | Standard Deviation |

|---|---|---|

| Female | 0.414 | 0.493 |

| Age 20 below | 0.016 | 0.126 |

| Age 20–39 | 0.379 | 0.485 |

| Age 40–59 | 0.503 | 0.500 |

| Age 60–79 | 0.093 | 0.290 |

| Age 80 and over | 0.009 | 0.093 |

| Any family history | 0.284 | 0.451 |

| Any heart problem | 0.089 | 0.285 |

| Diabetes | 0.015 | 0.120 |

| Overweight | 0.091 | 0.288 |

| Depression | 0.001 | 0.022 |

| Asthma | 0.029 | 0.168 |

| Cancer | 0.015 | 0.123 |

| Urban | 0.833 | 0.287 |

| Northeast | 0.168 | 0.374 |

| West | 0.266 | 0.442 |

| Midwest | 0.181 | 0.385 |

| South | 0.384 | 0.486 |

| Area Level Measures | ||

| Neighborhood Disadvantage Score | 0.005 | 0.926 |

| Less than High School | 15.0 | 0.107 |

| Unemployment Rate | 5.3 | 0.030 |

| Non-Managerial Employment | 62.2 | 0.131 |

| Poor | 10.8 | 0.080 |

| Near Poor | 15.2 | 0.076 |

| Vacancy Rate | 39.3 | 0.187 |

| Pollution | 41.388 | 12.140 |

| Mortgage Delinquency | 4.098 | 5.103 |

| Crime | 38.128 | 17.235 |

| Number of Zip Codes | 11241 | 20742 | p > |t| |

|---|---|---|---|

| Percent White | 75.0 | 85.0 | <0.001 |

| Percent Black | 10.2 | 6.1 | <0.001 |

| Percent Asian | 3.2 | 0.7 | <0.001 |

| Percent Hispanics | 9.8 | 5.0 | <0.001 |

| Percent No High School | 7.0 | 9.1 | <0.001 |

| Percent Some High School | 11.4 | 13.8 | <0.001 |

| Percent High School | 29.2 | 37.4 | <0.001 |

| Percent Some College | 27.5 | 25.2 | <0.001 |

| Percent College | 24.7 | 14.4 | <0.001 |

| Poverty Rate | 11.1 | 14.1 | <0.001 |

| Type of Policyholder | Stayers | Movers | p > |t| |

|---|---|---|---|

| Proportion | 78.24% | 21.76% | |

| Individual Characteristics | |||

| Female | 0.418 | 0.402 | 0.010 |

| Age 20 below | 0.015 | 0.019 | 0.003 |

| Age 20–39 | 0.356 | 0.446 | <0.001 |

| Age 40–59 | 0.524 | 0.452 | <0.001 |

| Age 60–79 | 0.096 | 0.076 | <0.001 |

| Age 80 and over | 0.008 | 0.006 | 0.018 |

| Any family history | 0.294 | 0.250 | <0.001 |

| Any heart problem | 0.094 | 0.073 | <0.001 |

| Diabetes | 0.015 | 0.013 | 0.188 |

| Overweight | 0.091 | 0.089 | 0.729 |

| Depression | 0.001 | 0.001 | 0.358 |

| Asthma | 0.029 | 0.029 | 0.983 |

| Cancer | 0.015 | 0.016 | 0.645 |

| Urban | 0.824 | 0.860 | <0.001 |

| Northeast | 0.171 | 0.156 | 0.002 |

| West | 0.264 | 0.279 | 0.006 |

| Midwest | 0.185 | 0.172 | 0.009 |

| South | 0.381 | 0.393 | 0.044 |

| Area Level Measures | |||

| Neighborhood Disadvantage Score | 0.005 | 0.003 | 0.852 |

| Less than High School | 15.0 | 14.9 | 0.265 |

| Unemployment Rate | 5.3 | 5.3 | 0.971 |

| Non-Managerial Employment | 62.6 | 61.3 | <0.001 |

| Poor | 10.8 | 10.8 | 0.865 |

| Near Poor | 14.9 | 14.9 | <0.001 |

| Vacancy Rate | 38.6 | 41.6 | <0.001 |

| Pollution | 41.134 | 42.477 | <0.001 |

| Mortgage Delinquency | 4.303 | 3.448 | <0.001 |

| Crime | 37.386 | 40.550 | <0.001 |

| Model Specification | Full Model (1) | Area Variables No Individual Variable (2) | Individual Variables Only (3) | Area Variables No Individual SES Variables (4) | ||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|---|

| Hazard Ratio | 95% Confidence Interval | Hazard Ratio | 95% Confidence Interval | Hazard Ratio | 95% Confidence Interval | Hazard Ratio | 95% Confidence Interval | |||||

| Neighborhood Disadvantage | 1.098 *** | 1.060 | 1.137 | 1.209 *** | 1.169 | 1.251 | 1.112 *** | 1.074 | 1.151 | |||

| Days PM2.5 over 40 Micrograms per cubic meter | 1.010 | 0.919 | 1.110 | 1.092 | 0.992 | 1.201 | 1.009 | 0.917 | 1.110 | |||

| Mortgage Delinquency Rate | 1.202 *** | 1.134 | 1.275 | 1.108 *** | 1.045 | 1.176 | 1.193 *** | 1.126 | 1.265 | |||

| Violent Crime Rate | 1.017 | 0.990 | 1.044 | 1.037 ** | 1.011 | 1.065 | 1.018 | 0.992 | 1.046 | |||

| Occupational Status (Manager is the reference) | ||||||||||||

| Financial | 0.955 | 0.832 | 1.096 | 0.953 | 0.830 | 1.095 | ||||||

| Science | 0.767 ** | 0.654 | 0.899 | 0.756 *** | 0.645 | 0.886 | ||||||

| Law/Social | 0.889 | 0.756 | 1.046 | 0.892 | 0.758 | 1.049 | ||||||

| Education | 0.815 ** | 0.704 | 0.943 | 0.817 | 0.706 | 0.946 | ||||||

| Protective Services | 0.908 | 0.723 | 1.140 | 0.920 | 0.733 | 1.156 | ||||||

| Health | 0.799 ** | 0.698 | 0.916 | 0.806 | 0.703 | 0.923 | ||||||

| Entertainment | 1.070 | 0.837 | 1.368 | 1.071 | 0.838 | 1.370 | ||||||

| Sales | 1.026 | 0.914 | 1.151 | 1.022 | 0.911 | 1.147 | ||||||

| Labor | 1.013 | 0.918 | 1.118 | 1.018 | 0.923 | 1.123 | ||||||

| Service | 1.097 | 0.954 | 1.262 | 1.099 | 0.955 | 1.263 | ||||||

| Not working | 1.185 * | 1.023 | 1.373 | 1.183 * | 1.022 | 1.370 | ||||||

| Other | 1.074 | 1.000 | 1.154 | 1.076 * | 1.002 | 1.156 | ||||||

| Income (less than $28,000 is the reference) | ||||||||||||

| $28,000 to 40,000 | 0.977 | 0.895 | 1.066 | 0.977 | 0.895 | 1.066 | ||||||

| $40,000 to 54,000 | 0.948 | 0.871 | 1.031 | 0.943 | 0.867 | 1.026 | ||||||

| $54,000 to 75,000 | 0.929 | 0.850 | 1.015 | 0.921 | 0.844 | 1.006 | ||||||

| $75,000 to 120,000 | 0.841 *** | 0.770 | 0.920 | 0.833 *** | 0.763 | 0.910 | ||||||

| Greater than 120,000 | 0.823 *** | 0.750 | 0.904 | 0.813 *** | 0.741 | 0.893 | ||||||

| Income Imputed Indicator | 1.076 | 0.996 | 1.163 | 1.064 | 0.985 | 1.150 | ||||||

| Female | 0.677 *** | 0.640 | 0.715 | 0.677 *** | 0.640 | 0.715 | 0.719 *** | 0.684 | 0.756 | |||

| Age (20–39 is the reference) | ||||||||||||

| Age <20 | 1.267 | 0.698 | 2.301 | 1.289 | 0.710 | 2.341 | 1.327 | 0.732 | 2.408 | |||

| Age 40–59 | 3.033 *** | 2.824 | 3.257 | 3.024 *** | 2.816 | 3.248 | 3.005 *** | 2.800 | 3.226 | |||

| Age 60–79 | 7.569 *** | 6.970 | 8.220 | 7.565 *** | 6.987 | 8.214 | 7.744 *** | 7.140 | 8.398 | |||

| Age 80+ | 14.34 *** | 12.410 | 16.550 | 14.55 *** | 12.61 | 16.79 | 14.51 *** | 12.66 | 16.63 | |||

| Any heart condition | 1.227 *** | 1.147 | 1.313 | 1.229 *** | 1.149 | 1.315 | 1.245 *** | 1.163 | 1.332 | |||

| Any cancer | 1.254 *** | 1.098 | 1.433 | 1.257 *** | 1.1000 | 1.436 | 1.257 *** | 1.100 | 1.435 | |||

| Any diabetes | 1.265 ** | 1.091 | 1.468 | 1.274 | 1.098 | 1.478 | 1.261 ** | 1.087 | 1.463 | |||

| % Black | 1.030 *** | 1.013 | 1.048 | 1.021 * | 1.004 | 1.038 | 1.062 | 1.08 | 1.076 | 1.032 *** | 1.015 | 1.049 |

| % Hispanic | 0.996 | 0.977 | 1.015 | 0.977 * | 0.959 | 0.996 | 1.036 *** | 1.20 | 1.052 | 0.999 | 0.980 | 1.018 |

| % Asian | 0.974 | 0.945 | 1.004 | 0.940 *** | 0.912 | 0.970 | 0.972 | 0.943 | 1.002 | 0.972 | 0.943 | 1.002 |

| % Native American/Other | 1.055 | 0.989 | 1.125 | 1.067 | 1.000 | 1.138 | 1.081 * | 1.015 | 1.151 | 1.056 | 0.990 | 1.126 |

| Model Specification | Full Model(1) | Area VariablesNo Individual Variables(2) | Individual Variables Only(3) | Area VariablesNo Individual SES Variables(4) | ||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|---|

| Hazard Ratio | 95% Confidence Interval | Hazard Ratio | 95% Confidence Interval | Hazard Ratio | 95% Confidence Interval | Hazard Ratio | 95% Confidence Interval | |||||

| Neighborhood Disadvantage | 1.145 *** | 1.082 | 1.212 | 1.251 *** | 1.200 | 1.303 | 1.164 *** | 1.100 | 1.232 | |||

| Days PM2.5 over 40 micrograms per cubic meter | 1.078 | 0.925 | 1.256 | 1.140 * | 1.019 | 1.275 | 1.079 | 0.926 | 1.257 | |||

| Mortgage Delinquency Rate | 0.972 | 0.891 | 1.060 | 0.989 | 0.921 | 1.062 | 0.958 | 0.878 | 1.044 | |||

| Violent Crime Rate | 1.078 *** | 1.034 | 1.125 | 1.054 *** | 1.021 | 1.087 | 1.080 *** | 1.035 | 1.126 | |||

| Occupational Status (Manager is the reference) | ||||||||||||

| Financial | 0.992 | 0.829 | 1.188 | 0.977 | 0.818 | 1.168 | ||||||

| Science | 0.750 ** | 0.617 | 0.911 | 0.738 ** | 0.608 | 0.897 | ||||||

| Law/Social | 0.753 | 0.567 | 1.001 | 0.760 | 0.568 | 1.015 | ||||||

| Education | 0.791 * | 0.645 | 0.969 | 0.797 * | 0.652 | 0.975 | ||||||

| Protective Services | 0.812 | 0.592 | 1.114 | 0.814 | 0.597 | 1.109 | ||||||

| Health | 0.769 ** | 0.648 | 0.913 | 0.767 ** | 0.646 | 0.911 | ||||||

| Entertainment | 1.082 | 0.772 | 1.514 | 1.088 | 0.782 | 1.515 | ||||||

| Sales | 1.076 | 0.923 | 1.254 | 1.062 | 0.912 | 1.237 | ||||||

| Labor | 0.975 | 0.849 | 1.119 | 0.972 | 0.847 | 1.115 | ||||||

| Service | 1.181 | 0.982 | 1.421 | 1.169 | 0.972 | 1.405 | ||||||

| Not working | 1.039 | 0.747 | 1.443 | 1.037 | 0.749 | 1.437 | ||||||

| Other | 1.123 | 1.016 | 1.242 | 1.120 | 1.014 | 1.237 | ||||||

| Income (less than $28,000 is the reference) | ||||||||||||

| $28,000 to 40,000 | 0.959 | 0.831 | 1.106 | 0.950 | 0.824 | 1.095 | ||||||

| $40,000 to 54,000 | 0.877 | 0.763 | 1.009 | 0.855 | 0.743 | 0.984 | ||||||

| $54,000 to 75,000 | 0.857 | 0.745 | 0.986 | 0.826 | 0.719 | 0.949 | ||||||

| $75,000 to 120,000 | 0.744 | 0.645 | 0.858 | 0.714 | 0.620 | 0.822 | ||||||

| Greater than 120,000 | 0.754 | 0.642 | 0.885 | 0.718 | 0.613 | 0.841 | ||||||

| Income Imputed Indicator | 1.284 | 1.119 | 1.472 | 1.297 | 1.132 | 1.485 | ||||||

| Female | 0.587 *** | 0.535 | 0.644 | 0.583 *** | 0.531 | 0.639 | 0.656 *** | 0.606 | 0.710 | |||

| Age (20–39 is the reference) | ||||||||||||

| Age <20 | 1.033 | 0.516 | 2.070 | 1.020 | 0.509 | 2.044 | 1.170 | 0.588 | 2.329 | |||

| Age 40–59 | 3.624 *** | 3.341 | 3.930 | 3.621 *** | 3.340 | 3.925 | 3.546 *** | 3.274 | 3.840 | |||

| Age 60–79 | 15.27 *** | 13.55 | 17.21 | 15.28 *** | 13.56 | 17.21 | 15.30 *** | 13.62 | 17.18 | |||

| Age 80+ | 107.1 *** | 67.48 | 170.0 | 110.8 *** | 70.06 | 175.3 | 108.2 *** | 69.39 | 168.8 | |||

| Any heart condition | 1.347 *** | 1.198 | 1.514 | 1.346 *** | 1.197 | 1.512 | 1.374 *** | 1.222 | 1.545 | |||

| Any cancer | 1.508 ** | 1.148 | 1.980 | 1.475 ** | 1.118 | 1.946 | 1.481 ** | 1.102 | 1.990 | |||

| Any diabetes | 1.394 ** | 1.093 | 1.778 | 1.393 ** | 1.095 | 1.0772 | 1.396 ** | 1.097 | 1.077 | |||

| % Black | 1.035 * | 1.005 | 1.065 | 1.026 * | 1.004 | 1.048 | 1.084 *** | 1.059 | 1.109 | 1.036 * | 1.006 | 1.067 |

| % Hispanic | 0.998 | 0.969 | 1.027 | 0.973 * | 0.951 | 0.996 | 1.039 ** | 1.016 | 1.064 | 1.003 | 0.975 | 1.033 |

| % Asian | 0.963 | 0.923 | 1.004 | 0.929 *** | 0.896 | 0.964 | 0.950 | 0.909 | 0.992 | 0.959 | 0.919 | 1.002 |

| % Native American/Other | 1.103 | 0.968 | 1.256 | 1.130 ** | 1.033 | 1.236 | 1.160 * | 1.019 | 1.319 | 1.108 | 0.978 | 1.255 |

| Model Stratification (Unweighted and Weighted) | Hazard. Ratio | p >|t| | 95% Confidence Interval | |

|---|---|---|---|---|

| A. Unweighted | ||||

| All Policyholders | 1.098 *** | <0.001 | 1.060 | 1.137 |

| Stayers | 1.078 *** | <0.001 | 1.036 | 1.122 |

| Movers | 1.171 *** | <0.001 | 1.086 | 1.262 |

| B. Weighted | ||||

| All Policyholders | 1.145 *** | <0.001 | 1.082 | 1.212 |

| Stayers | 1.115 *** | 0.001 | 1.045 | 1.188 |

| Movers | 1.234 *** | <0.001 | 1.103 | 1.381 |

| Models Stratified by Income (Weighted and Unweighted) | Hazard. Ratio | p >|t| | 95% Confidence Interval | |

|---|---|---|---|---|

| A. Unweighted | ||||

| <$40,000 | 1.066 * | 0.044 | 1.002 | 1.134 |

| $40,000–$75,000 | 1.113 ** | 0.003 | 1.037 | 1.194 |

| >$75,000 | 1.118 ** | 0.002 | 1.042 | 1.198 |

| B. Weighted | ||||

| <$40,000 | 1.096 | 0.077 | 0.990 | 1.213 |

| $40,000–$75,000 | 1.127 * | 0.020 | 1.019 | 1.246 |

| >$75,000 | 1.181 ** | 0.001 | 1.066 | 1.309 |

© 2019 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (http://creativecommons.org/licenses/by/4.0/).

Share and Cite

Gaskin, D.J.; Roberts, E.T.; Chan, K.S.; McCleary, R.; Buttorff, C.; Delarmente, B.A. No Man is an Island: The Impact of Neighborhood Disadvantage on Mortality. Int. J. Environ. Res. Public Health 2019, 16, 1265. https://0-doi-org.brum.beds.ac.uk/10.3390/ijerph16071265

Gaskin DJ, Roberts ET, Chan KS, McCleary R, Buttorff C, Delarmente BA. No Man is an Island: The Impact of Neighborhood Disadvantage on Mortality. International Journal of Environmental Research and Public Health. 2019; 16(7):1265. https://0-doi-org.brum.beds.ac.uk/10.3390/ijerph16071265

Chicago/Turabian StyleGaskin, Darrell J., Eric T. Roberts, Kitty S. Chan, Rachael McCleary, Christine Buttorff, and Benjo A. Delarmente. 2019. "No Man is an Island: The Impact of Neighborhood Disadvantage on Mortality" International Journal of Environmental Research and Public Health 16, no. 7: 1265. https://0-doi-org.brum.beds.ac.uk/10.3390/ijerph16071265